How Automation Is Reshaping Europe’s Food Industry

Why smart factories, robotics, and AI-led processing are becoming essential for the future of food manufacturing in Europe

Across the continent, food manufacturers are under pressure from all directions. Consumers want more processed, packaged, ready-to-eat, and convenience foods. Governments are demanding stricter food safety, hygiene, and traceability standards. Businesses are battling labor shortages, rising operational costs, and growing competition. In response, the industry is doing what many sectors across Europe are doing: investing in automation.

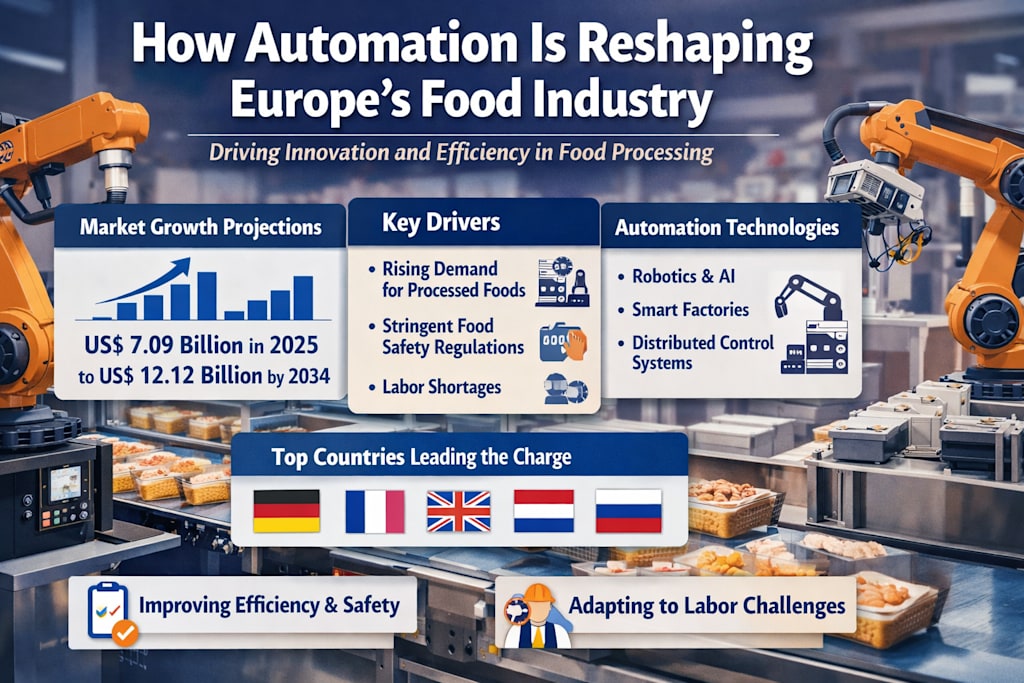

According to Renub Research, the Europe Food Processing Automation Market is projected to grow from US$ 7.09 billion in 2025 to US$ 12.12 billion by 2034, expanding at a CAGR of 6.14% during 2026–2034. That growth reflects more than technology adoption—it reflects a major structural shift in how food is made, packed, inspected, and delivered across Europe.

This transformation is not happening in isolated high-tech factories. It is spreading across dairy plants, bakery lines, meat processing units, beverage facilities, packaging stations, and regional food operations. Automation is no longer a futuristic concept in food production. It is fast becoming a practical necessity.

What Food Processing Automation Really Means

At its core, food processing automation is the use of machines, robotics, control systems, sensors, software, and intelligent equipment to carry out food manufacturing tasks that were once done manually or semi-manually.

That includes operations such as:

Sorting raw ingredients

Slicing and cutting

Mixing and blending

Heating and cooking

Filling and packaging

Labelling and palletizing

Quality inspection and traceability monitoring

The benefit is straightforward: automation allows food producers to manufacture at scale while maintaining consistency, hygiene, efficiency, and speed. It also reduces human error, lowers contamination risk, and supports round-the-clock production cycles. Europe’s food companies increasingly see automation not as an upgrade, but as an operational backbone.

The Processed Food Boom Is Driving Investment

One of the biggest reasons behind this market growth is the simple fact that Europeans are buying more convenience food.

Busy lifestyles, dual-income households, urban living, and changing eating habits have all contributed to stronger demand for packaged foods, frozen meals, bakery products, dairy snacks, functional drinks, and ready-to-cook items. Consumers want convenience—but they also expect consistency, freshness, and safe packaging.

That puts enormous pressure on food manufacturers.

Traditional, labor-heavy systems struggle to keep up with this demand while maintaining quality at scale. Automated production lines, however, are designed for exactly this kind of challenge. They can process high volumes continuously, standardize output, and reduce waste.

This is especially important in categories where product quality must remain consistent across every unit—whether it’s yogurt, sliced cheese, prepared salad, frozen vegetables, or packaged bakery items. As product demand diversifies, automation helps producers adapt quickly without sacrificing speed or compliance.

Food Safety Rules Are Making Automation More Valuable

In Europe, food safety is not optional. It is tightly regulated, heavily monitored, and central to consumer trust.

That is why automation is increasingly being viewed as a food safety tool, not just a productivity tool.

Automated systems reduce the amount of direct human contact with food during production, packaging, and inspection. This improves hygiene and lowers the risk of contamination. Sensors and digital monitoring systems also help manufacturers maintain temperature control, batch traceability, process consistency, and cleaning compliance.

As regulatory frameworks evolve, food manufacturers are under pressure to document every stage of production more accurately. Automation makes this easier by creating digital records and process visibility across the entire production chain.

For companies operating in high-compliance sectors such as dairy, meat, beverages, and ready meals, automated systems are becoming critical for maintaining both regulatory compliance and consumer confidence.

Europe’s Labor Crisis Is Accelerating Automation

One of the most powerful forces behind food automation in Europe is the labor challenge.

Food processing often relies on repetitive, physically demanding, and shift-based work. These roles are increasingly difficult to fill, particularly in industrial and semi-rural areas. At the same time, wage costs are rising and skilled labor shortages are affecting factory productivity.

That has made automation economically attractive.

Machines do not take sick leave, require shift premiums, or create staffing bottlenecks during peak demand seasons. Once installed, automated systems can run continuously, helping manufacturers reduce long-term labor dependency and improve operational efficiency.

This does not mean the food industry is becoming worker-free. Instead, it is becoming worker-different. More companies now need technicians, maintenance specialists, software operators, and digital process managers alongside line workers.

In that sense, automation is not just changing how food is made—it is changing the very nature of food manufacturing jobs across Europe.

Smart Factories and Industry 4.0 Are Entering Food Production

Europe’s automation push is also being shaped by a broader industrial trend: Industry 4.0.

Food factories are increasingly integrating connected systems, sensors, robotics, data monitoring, and predictive maintenance tools into their production environments. Instead of operating as isolated machines, modern automation systems are becoming part of an intelligent, data-driven production ecosystem.

This is particularly useful in food manufacturing, where downtime is expensive and product loss can be significant.

Smart automation enables manufacturers to:

Track machine performance in real time

Predict maintenance before equipment failure

Monitor energy usage

Improve production scheduling

Reduce waste and improve throughput

Respond faster to changing product formats or packaging needs

This shift is turning food plants into smarter, more responsive environments—especially in countries with advanced manufacturing ecosystems like Germany, France, and the UK.

Why Distributed Control Systems Matter

A major technology segment within this market is the Distributed Control Systems (DCS) category.

DCS platforms help food manufacturers centrally monitor and control different stages of the production line—from raw material handling and cooking to packaging and final quality checks. These systems are especially useful in complex or continuous production environments where consistency is essential.

For European food manufacturers, DCS brings several advantages:

Better control over multiple production stages

Improved product consistency

Reduced downtime

Stronger traceability

Better energy optimization

Easier compliance reporting

This is particularly relevant in high-volume sectors such as dairy, beverages, and ready meals, where multiple temperature-sensitive and time-sensitive steps must work together with precision.

Hardware Is the Backbone of Food Automation

While software often gets the spotlight, automation depends heavily on physical systems.

The European food processing automation hardware market includes:

Food-grade robots

Sensors and transmitters

Controllers

Conveyor systems

Actuators and valves

Electric motors

Machine vision systems

These are the components that keep lines moving, monitor quality, and ensure reliable performance in demanding processing environments.

Because food manufacturing requires hygienic and durable equipment, hardware design in Europe increasingly focuses on easy cleaning, corrosion resistance, maintenance efficiency, and precision performance. Smart sensors and advanced robotic systems are especially gaining traction, helping companies improve accuracy and reduce waste during high-speed operations.

Dairy and Packaging Are Leading the Automation Race

Among end-use sectors, dairy processing remains one of the strongest adopters of automation in Europe.

That makes sense. Dairy products require high levels of cleanliness, precise temperature control, fast processing, and contamination prevention. Automation supports everything from pasteurization and fermentation to filling and packaging.

As European demand grows for cheese, yogurt, functional dairy drinks, and premium dairy products, processors are under pressure to maintain product quality while scaling efficiently. Automation is helping them do exactly that.

At the same time, packaging and re-packaging is emerging as another major growth area.

Today’s food market is driven by branding, sustainability, smaller portions, private labels, multilingual labelling, and retail customization. Automated packaging systems allow manufacturers to fill, seal, label, sort, and palletize products with greater speed and flexibility.

This is especially important in Europe, where changing consumer expectations and retail competition demand faster packaging adaptation than ever before.

Fully Automatic vs. Semi-Automatic: Two Paths, One Goal

Not every food processor in Europe is moving at the same pace—and that is shaping the market in interesting ways.

Fully Automatic Systems

Large manufacturers are increasingly investing in fully automatic food processing lines. These systems minimize human intervention, increase throughput, improve hygiene, and support standardized production. While the upfront investment is high, the long-term operational savings can be significant.

For major brands and export-oriented manufacturers, fully automated lines are becoming a competitive advantage.

Semi-Automatic Systems

At the same time, semi-automatic systems remain highly relevant—especially for small and medium-sized processors, specialty food producers, and artisanal brands.

These systems offer a balance between flexibility and efficiency. They allow businesses to automate key steps without fully replacing existing infrastructure. For niche producers, regional manufacturers, and budget-conscious operations, semi-automation is often the most realistic and strategic path forward.

Which Countries Are Leading?

Several European countries are playing major roles in this market’s evolution.

Germany

Germany stands out as one of the most advanced food processing automation markets in Europe. Its strength lies in engineering expertise, industrial digitization, and early adoption of Industry 4.0. German food manufacturers are using automation extensively in meat processing, confectionery, beverages, and ready meals.

France

France’s strong food and beverage tradition is helping drive automation adoption, particularly in dairy, bakery, meat, and beverage production. Manufacturers are investing in scalable systems to improve purity, consistency, and efficiency while reducing waste and energy use.

United Kingdom

The UK market is increasingly focused on automation to address workforce shortages and maintain stable production. Packaging, sorting, and inspection technologies are especially important in sectors like bakery, meat, and ready meals.

Russia and Broader Europe

Other markets, including Russia and several Eastern and Southern European countries, are gradually increasing adoption as local production capacity grows and manufacturers seek long-term efficiency gains.

The Competitive Landscape

The market includes a strong lineup of industrial automation and engineering players, including:

ABB Ltd.

Alfa Laval AB

Bosch Rexroth AG

Bühler Holding AG

Emerson Electric Co.

FANUC Corp.

Festo SE & Co. KG

Endress+Hauser Group Services AG

Baader Food Processing Machinery GmbH

These companies are helping food manufacturers modernize operations with a mix of robotics, sensors, processing systems, digital monitoring tools, and automation infrastructure.

Final Thoughts

Europe’s food processing automation market is not growing because automation is fashionable. It is growing because the food industry is facing a very real operational reset.

Consumers want more convenience. Regulators want better traceability. Manufacturers want lower waste, better margins, and stronger consistency. Workers are harder to find. Costs are harder to control.

About the Creator

Keep reading

More stories from shibansh kumar and writers in Trader and other communities.

United States Thermoplastic Polyurethane Market Set for Strong Growth Through 2034

When people think about materials shaping the future of American manufacturing, they often imagine semiconductors, batteries, or advanced composites. Yet one of the most versatile and commercially important materials expanding across U.S. industries is thermoplastic polyurethane, better known as TPU.

By shibansh kumarabout 6 hours ago in Trader

Philippines Tire Market 2026: Replacement Demand, Two-Wheeler Growth & Smart Tire Technologies

Philippines Tire Market Overview The Philippines tire market is a steadily growing segment of the country’s automotive and transportation ecosystem, supplying essential components for passenger vehicles, commercial fleets, two-wheelers and off-road machinery. Tires play a critical role in ensuring vehicle safety, performance and fuel efficiency, making them a key component of both OEM and replacement markets.

By Manisha Dixit6 days ago in Trader

Low Voltage Electric Motor Market Outlook 2034: Driving Efficiency Across Industrial and Commercial Applications

Overview Low Voltage Electric Motor Market The low voltage electric motor market forms an essential part of the global electrical equipment and industrial machinery sector. These motors typically operate at voltages up to 1,000 volts and are widely used across industries due to their reliability, cost-effectiveness, and versatility. They are commonly found in applications such as pumps, compressors, fans, conveyors, and various automated systems.

By James Smitha day ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.